A product case study of how a former debt collection Product manager built a tool to empower consumers with insider knowledge and actionable steps to challenge unfair debt collection practices

The Problem: Debt Collection is Unfair

Everyone knows debt is complicated, but here’s what most don’t realize: the debt collection system is fundamentally designed to exploit consumer confusion and shame.

Over 70 million Americans have debts in collections, yet only a tiny fraction know their rights or how to effectively dispute questionable claims. The statistics are staggering:

- 35% of American adults with credit files have debts in collection

- 44% of consumers report feeling “scared,” “confused,” or “helpless” when contacted by collectors

- Only 1 in 20 consumers dispute a debt, despite studies showing that up to 59% of debt portfolios contain inaccuracies

- The average consumer spends 45+ hours trying to resolve debt-related issues

And when we talk to these consumers, a clear pattern emerges: they’re not looking for shortcuts or ways to dodge legitimate obligations. They simply want clarity, fairness, and a way to challenge mistakes.

This is exactly where DebtCat founder Lyor saw a profound market gap. As someone who had worked inside the debt collection industry, he had unique insight into how the system operates—and how consumers could level the playing field.

The Vision: Democratizing Debt Knowledge Without the Subscriptions

“When I worked in collections, I saw firsthand how disempowered consumers feel,” explains Lyor. “People in my community started asking for help navigating the system. That’s when I realized: what if everyone had access to insider knowledge about how to handle debt collectors?”

DebtCat’s vision crystallized around a simple but powerful concept: a “first aid kit for consumers in debt” that demystifies the process and provides practical tools without expensive subscriptions or counseling plans.

Unlike most fintech products targeting debt, DebtCat deliberately avoids:

- Requiring sign-ups or storing personal information

- Pushing subscription models

- Offering general advice without actionable steps

- Focusing on debt consolidation (which often just shifts debt around)

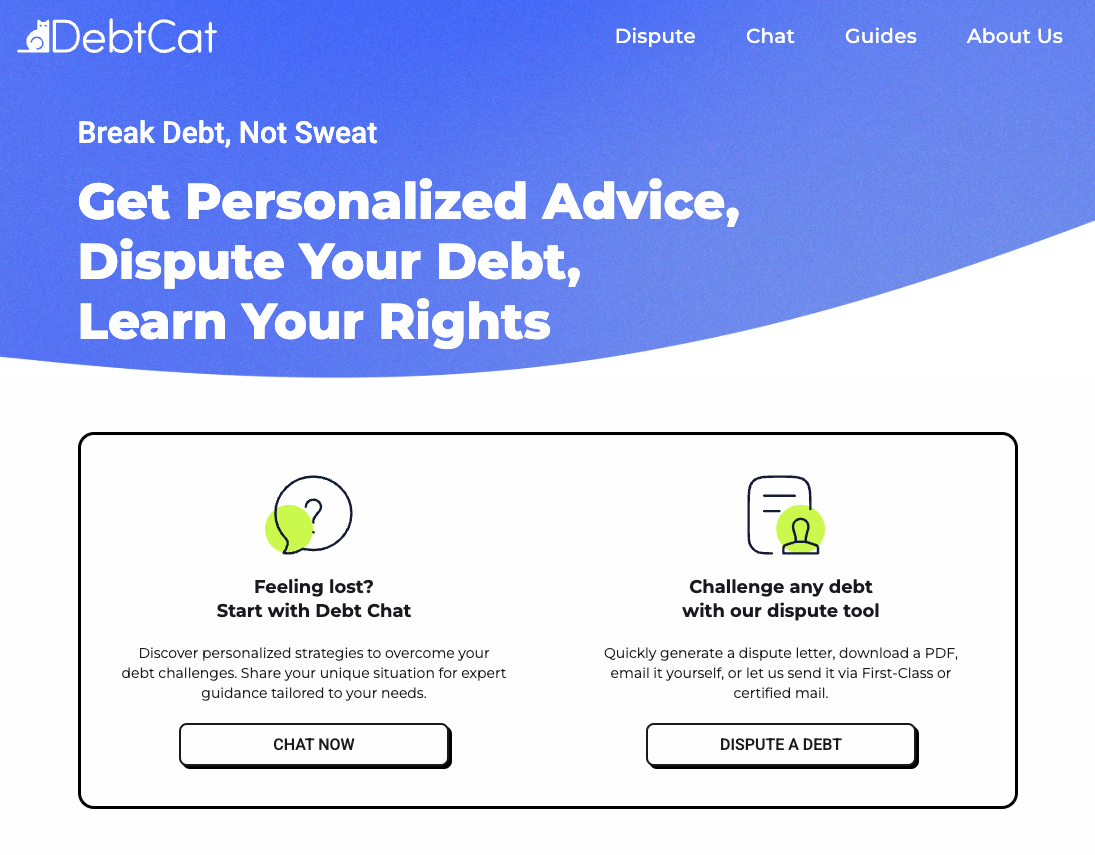

Instead, DebtCat focuses on three core pillars:

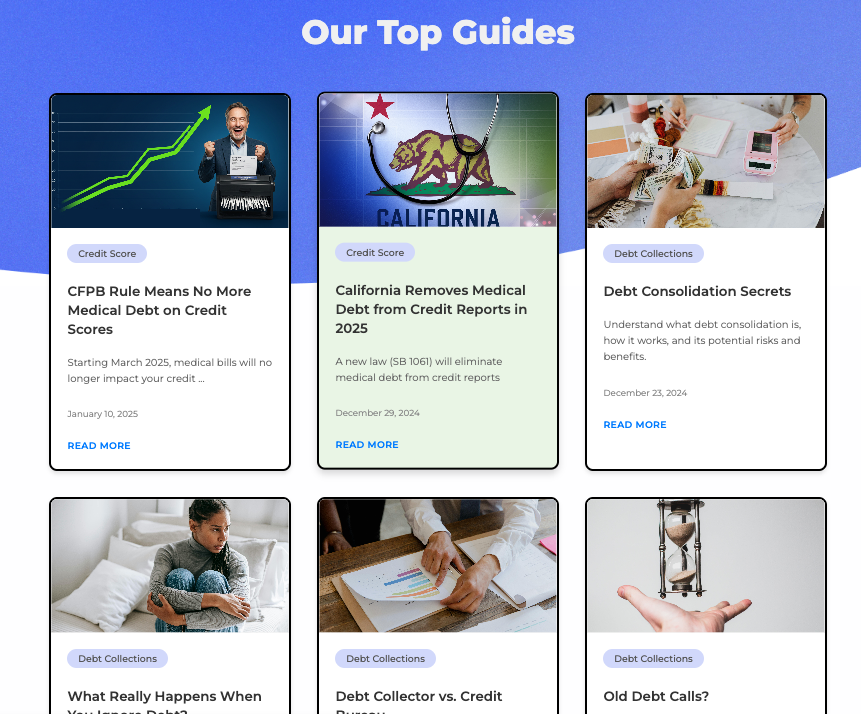

- Education: Clear, jargon-free guides about consumer rights

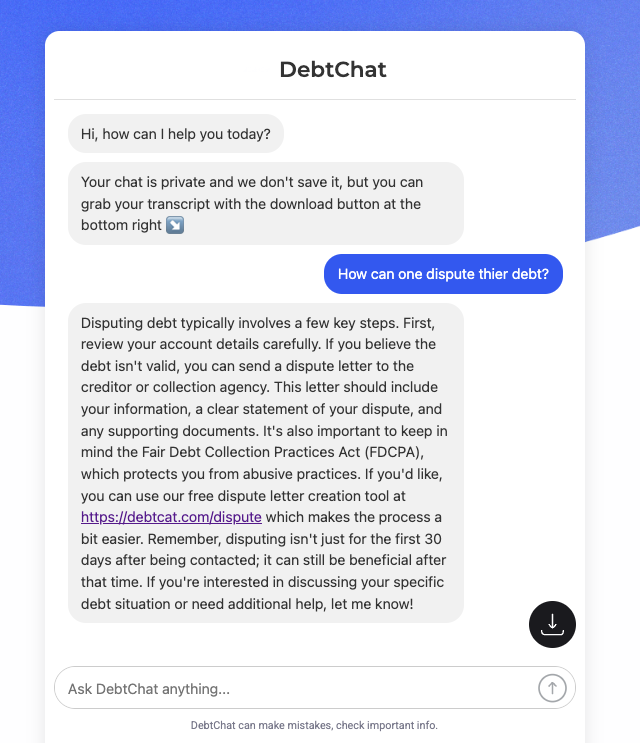

- Conversation: An AI chatbot that answers specific questions

- Action: A dispute letter generator that creates legally-sound communications

The Journey: From WordPress to Firebase (with Some Technical Debt)

Building DebtCat was as much about product decisions as it was about technical flexibility. The journey through three different tech stacks illustrates how early-stage products often need to pivot quickly based on changing requirements.

“I started with WordPress and Elementor because it was the fastest way to get content online,” says Lyor. “But as soon as we hired design talent, we realized we needed more design flexibility.”

Tech Stack Evolution

Phase 1: WordPress + Elementor

Strengths:

- Fast launch

- Familiar CMS

Weaknesses:

- Design limitations

- Performance issues

Phase 2: Webflow

Strengths:

- Superior design control

- Visual editing

Weaknesses:

- Cost (especially as content grew)

- Limited technical extensibility

Phase 3: Firebase

Strengths:

- Scalable

- Low cost

- Better developer control

Weaknesses:

- Lost CMS functionality

- Required rebuilding components

“The choice to move from Webflow to Firebase was financially driven,” explains Lyor. “We were paying for capabilities we didn’t need yet, and I wanted to allocate resources to user acquisition.”

Building Solo with AI as a Force Multiplier

What makes the DebtCat story particularly interesting from a product development perspective is how AI tools enabled a non-developer to build and deploy a sophisticated web application.

“A few years ago, building DebtCat would have required a full development team,” notes Lyor. “But with the advances in AI coding assistants, I was able to leverage tools like ChatGPT, Cursor, and Windsurf to accelerate development dramatically.”

The AI development process followed a consistent pattern:

- Planning: Define the feature and user flow using traditional PM methods

- Component Design: Use AI to generate baseline HTML/CSS components

- Integration: Leverage AI to connect components and add functionality

- Debugging: Use AI to identify and fix issues in the implementation

“The AI didn’t replace product thinking,” Lyor emphasizes. “But it did reduce the technical barrier to implementation. I could focus on ‘what should we build?’ rather than getting stuck on ‘how do I write this code?’”

Product Design: Optimizing for Trust and Low Friction

For a product dealing with sensitive financial information, building trust while minimizing friction presented a unique challenge:

- No Account Creation: Users can generate dispute letters without creating an account or storing data

- Progressive Disclosure: Information is presented in bite-sized chunks to avoid overwhelming users

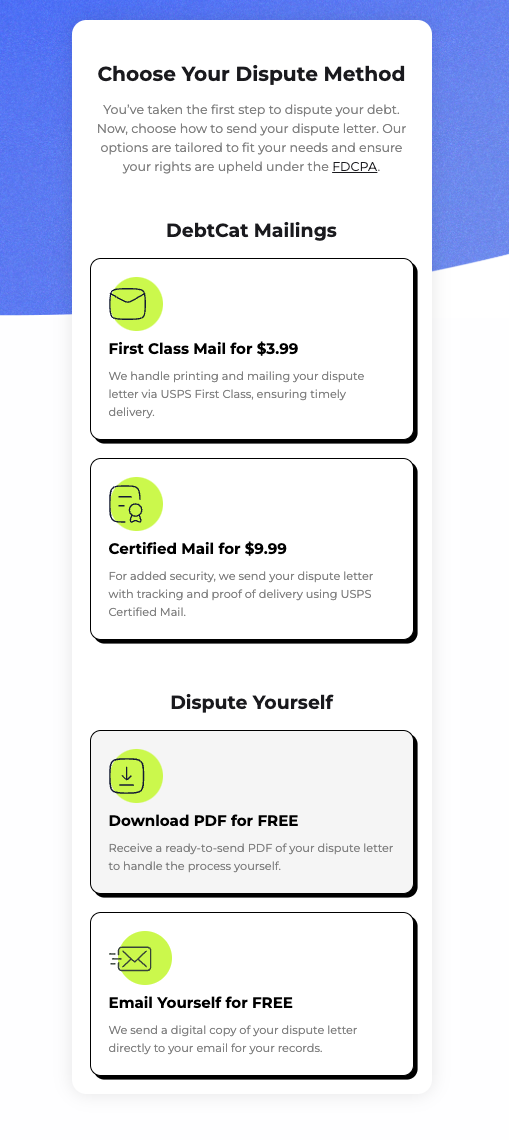

- Transparent Business Model: Clear pricing only for premium features (mailing services)

- Education-First Approach: Deep content library builds credibility before asking users to take action

“Our biggest design insight was that users needed to feel safe before they’d engage,” says Dalma, the product designer. “We removed as many friction points as possible, even if it meant sacrificing some ‘nice-to-have’ features.”

Key Challenges: Doubt, Distribution, and Technical Debt

1. Credibility in a Sea of Scams

The debt relief space is notoriously filled with predatory services. Establishing DebtCat as a legitimate, consumer-friendly alternative required careful positioning.

“We had to overcome the inherent skepticism people have around debt products,” explains Lyor. “This influenced everything from our messaging to our refusal to ask for payment information upfront.”

2. Distribution Roadblocks

“Email service providers were hesitant to work with us because we mentioned ‘debt’ in our content,” says Lyor. “Even Google presented similar challenges with our ads. We never expected that helping consumers would trigger the same red flags as predatory lending!”

This forced the team to rely heavily on social channels and direct community engagement rather than conventional growth tactics.

3. Technical Constraints and Tradeoffs

“When we migrated from Webflow to Firebase, many styling features and CMS-related articles broke,” recalls Lyor. “I spent a weekend rebuilding headers, footers, and article pages, knowing I was accumulating technical debt for the sake of speed.”

Lessons for Product Leaders

1. Insider Knowledge Creates Unique Product Opportunities

Lyor’s experience in collections gave him perspective that would be difficult to acquire through traditional market research. Domain expertise revealed both the problem and the solution in ways that might not be obvious to outsiders.

Takeaway: Look for product opportunities where your unique background gives you insight others might miss.

2. Technical Stack Should Follow Product Needs, Not Vice Versa

The willingness to migrate between three platforms demonstrates how product requirements should drive technical decisions, not the other way around.

Takeaway: Be ready to change technical direction when product needs evolve, even if it means short-term inconvenience.

3. AI Tools Are Changing the Product Development Equation

The ability to build DebtCat with minimal development resources highlights how AI is democratizing technical implementation.

Takeaway: AI-assisted development can allow product thinkers to build with less technical dependency, but only when the vision is clear.

4. Consumer Trust Comes Before Monetization

By prioritizing trust over immediate monetization, DebtCat built a foundation for sustainable growth in a highly skeptical market.

Takeaway: In sensitive domains, establishing trust is worth sacrificing short-term revenue opportunities.

What’s Next: The Roadmap Ahead

DebtCat’s future plans focus on expanding capabilities while maintaining the core commitment to accessibility:

- Negotiation Features: Adding tools that help users negotiate directly with collectors

- Credit Report Integration: Allowing users to pull credit reports so they can see all their debts in one place

- Expanded Education: Creating more targeted content for specific debt situations

- Ethical Partnerships: Forming alliances with reputable debt consolidation and credit counseling services

The team is also exploring the possibility of converting DebtCat into a nonprofit to broaden its reach and impact.

“The debt collection industry isn’t going to change overnight,” says Lyor. “But by empowering consumers with the right tools and knowledge, we can help level the playing field one dispute at a time.”

Try It Yourself

DebtCat is available at debtcat.com, and all core features are free to use without signup. Whether you’re dealing with debt personally or know someone who is, it’s worth exploring as a resource.